Evidence for additional foreigner acquirer duty exemption application

These guidelines detail the evidence and documents you need when applying for an exemption from AFAD for residential land developers.

Residential land developers may be eligible for an exemption from additional foreign acquirer duty (AFAD) for transactions entered into on or after 15 December 2025.

The public ruling on this exemption (GEN012) sets out the administrative arrangement, including an explanation of terminology and requirements. The information and examples below are the Commissioner of State Revenue’s guidelines on the general information you need when applying for the exemption.

- These guidelines provide general information and do not override the ruling.

- Each application is considered on a case-by-case basis.

- An incomplete application may cause delays in determining your eligibility for the exemption.

- Where possible, we’ll use the information we have but may request additional information from you.

Eligibility

We will generally consider the facts and circumstances as at the date the liability for transfer duty arises for the land the subject of the exemption, which is usually the date of the contract. Where relevant, we may also consider the period immediately before that date.

You need to provide evidence that you have satisfied certain conditions.

You must prove that you meet:

- Australian-based requirements

- Foreign Investment Review Board (FIRB) requirements

- regulatory requirements

- developer requirements.

General requirements

See the public ruling (GEN012) for the full list of defined terms.

An entity is an individual or company registered under the Corporations Act 2001 (Cwlth).

Where an entity is a trustee acting in a nominee or custodian capacity for regulatory compliance purposes, the nominee or custodian will be looked through and eligibility will be determined by the activities of the next-level trustee.

Corporate group tracing is available for most of the eligibility requirements in the ruling.

- A parent entity is an entity that directly owns at least 90% of the issued shares in and has voting control over another entity.

- A subsidiary entity (first entity) is one in which another entity directly owns at least 90% of issued shares and has voting control over the first entity.

- Voting control means that an entity is in a position to cast, or control the casting of, 90% or more of the maximum votes that can be cast at a general meeting of a company (other than under a debenture or trust deed securing the issue of a debenture).

- All parent and subsidiary entities constitute a corporate group.

- Each entity within the corporate group is a group entity.

The circumstances and activities of a group entity can be taken into account when considering whether relevant requirements are satisfied. Where this happens, the entity is referred to as a ‘relevant group entity’.

Supporting documentation includes:

- a corporate structure diagram of the corporate group confined to entities that are directly connected by at least 90% share-ownership and voting control (including identifying the entity seeking the exemption and the other group entities)

- ASIC records confirming the entity’s connection with the parent entity that directly owns at least 90% of its shares and any other entity being relied on via corporate group tracing, in the 12-months before the liability date

- information confirming that these connections and arrangements existed at the date the liability for transfer duty arises for the land the subject of the exemption

- information confirming how the relevant group entity is satisfying the nominated requirement in connection with the land the subject of the exemption.

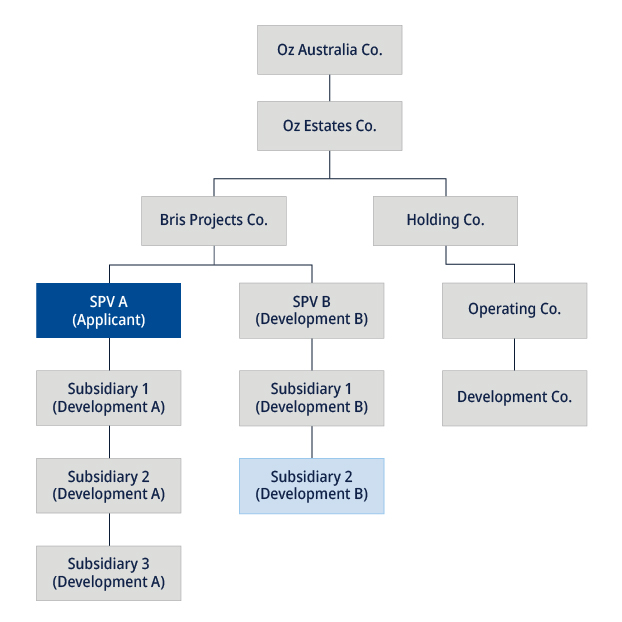

Example: Corporate group connected by 90% or more shareholding and voting control

SPV A has applied for an exemption for AFAD residential land it acquired on 31 January 2026. This is also the date that SPV A became liable for transfer duty (including AFAD) on the acquisition of the land (liability date). SPV A does not meet the Australian-based requirements at the liability date, except for having an Australian head office and Australian principal place of business.

However, Subsidiary 2 (Development B) has provided information to confirm that it is connected to SPV A through the other entities in the corporate group by way of 90% or more shareholding and voting control at the liability date. That is, as defined under the ruling:

- SPV A is the subsidiary of Bris Projects Co.; and Bris Projects Co. is a parent of SPV A.

- Bris Projects Co. is the parent of SPV B; and SPV B is a subsidiary of Bris Projects Co.

- SPV B is a parent of Subsidiary 1 (Development B); and Subsidiary 1 (Development B) is a subsidiary of SPV B.

- Subsidiary 1 (Development B) is a parent of Subsidiary 2 (Development B); and Subsidiary 2 (Development B) is a subsidiary of Subsidiary 1 (Development B).

- SPV A, Bris Projects Co., SPV B, Subsidiary 1 (Development B) and Subsidiary 2 (Development B) are a relevant corporate group at the liability date.

Subsidiary 2 (Development B) has also provided information to confirm that it meets the Australian-based requirements as at the liability date. On this basis, the Australian-based requirements for SPV A’s exemption application are met.

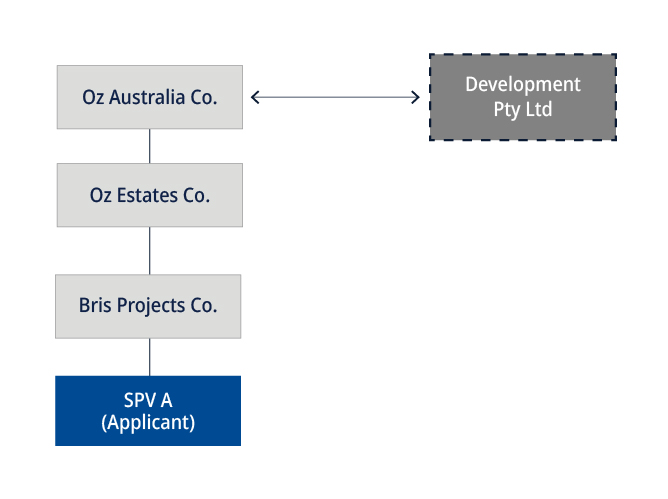

Example: Use of contractors to undertake development activities

SPV A is the landholding entity and applicant. It is not undertaking any development in its own right, but is holding the land passively.

Under the ruling:

- Oz Australia Co. is a parent of Oz Estates Co.; and Oz Estates Co. is a subsidiary.

- Oz Estates Co. is a parent of Bris Projects Co.; and Bris Projects Co. is a subsidiary.

- Bris Projects Co. is a parent of SPV A; and SPV A is a subsidiary.

- These entities constitute a relevant corporate group.

- Oz Australia Co. engages Development Pty Ltd to undertake residential development activities on SPV A’s land. Development Pty Ltd expects to build 100 residential lots within 6 months of the liability date.

- Development Pty Ltd is not part of the relevant corporate group. It is neither a parent nor a subsidiary for Oz Australia Co., Oz Estates Co, Bris Projects Co. or SPV A.

- Given that Development Pty Ltd is not part of the relevant corporate group, its development activities on SPV A’s land cannot be counted.

See the public ruling (GEN012) for definition of ‘notifiable event’.

The notification requirement continues until:

- a minimum of 20 residential lots has been developed or re-developed—for the qualifying development test

- at the end of the summing period or averaging period (whichever is later)—for the large developer test.

We have used future dates in these examples.

Example: Corporate group changes before liability arises

GFL Pty Ltd received pre-approval on 30 September 2026. Pre-approval was sought on 10 September 2026 for land GFL expects to acquire on 10 April 2027.

GFL received pre-approval on the basis that a group entity, JJJ Pty Ltd, had been approved for the AFAD exemption previously. The evidence confirmed that JJJ was GFL’s parent at the time pre-approval was sought, owning 95% of the shares as well as 95% voting control in GFL.

On 1 January 2027, JJJ disposed of all of its shares and voting control in GFL. This means that JJJ is no longer a group entity.

Consequently, GFL is required to notify the Commissioner of this change in the approved form. Further, GFL may need to apply for pre-approval on a different basis or apply for the AFAD exemption without pre-approval when the liability for transfer duty arises for the acquisition on 10 April 2027.

Example: Corporate group changes after exemption received but before development requirements have been satisfied

BBB Pty Ltd received the AFAD exemption for land it acquired on 20 July 2027 on the basis that its corporate group is a large developer as defined in the ruling. As part of its application for the exemption, BBB submitted that its group entity, CCC Pty Ltd, would build 30 residential lots on the land between 1 September 2027 and 1 September 2028 (the summing period).

In obtaining the exemption, it was confirmed that BBB was CCC’s parent in the period immediately before, and on the date transfer duty liability arises (20 July 2027). In particular, on this date, BBB owned 95% of the shares as well as 95% voting control in CCC.

On 1 January 2027, BBB disposed of all of its shares and voting control in CCC. This means that CCC is no longer a group entity. CCC had only constructed 10 residential lots on the land when this change arose.

Consequently, BBB is required to notify the Commissioner of this change in the approved form. Further, unless any additional developments or other qualifying criteria apply, BBB is likely to need to repay the amount of AFAD exemption received.

Example: Development requirements not met after qualifying development exemption applied

DDD Pty Ltd received the AFAD exemption for land it acquired on 10 June 2027 on the basis that the land subject of the transaction was a qualifying development as defined in the ruling. As part of its application for the exemption, DDD submitted that it would build 25 residential lots on the land between 1 July 2027 and 30 June 2028.

During this period, DDD rearranged its affairs and limited its development to 15 residential lots. DDD continued to maintain possession of the land after the period had ended.

Consequently, DDD is required to notify the Commissioner of this change in the approved form. Further, unless any additional developments or other qualifying criteria apply, DDD is likely to need to repay the amount of AFAD exemption received.

An entity can apply for pre-approval for the AFAD exemption if one of the following applies:

- The entity has previously been approved for the AFAD exemption (or AFAD ex gratia relief).

- A group entity in a corporate group has been approved for the AFAD exemption while a member of the group, and the entity is the parent or a subsidiary of the group entity when the liability for transfer duty arises (the AFAD liability date).

If pre-approval is given, it will continue to apply until a notifiable event occurs.

A lot includes individual dwellings that are independently habitable by a single family unit and is not limited to the meaning of a lot under the Land Title Act 1994.

Land lease communities (LLCs) may meet the development requirements. For these cases, we will generally look to see whether a requisite number of individual sites (each for a single dwelling) will be produced, rather than a requisite number of separately titled lots. Other examples of a lot may include:

- an independent living unit (ILU) in a retirement village

- a site in a residential park

- a dwelling in a built-to-rent development. See section 58D of the Land Tax Act 2010.

An entity is not eligible for the AFAD exemption for a relevant transaction if the amount of AFAD on the transaction has been calculated under Chapter 4, Part 4AA of the Duties Act 2001 (concessions for eligible BTR developments).

Australian-based requirements

Generally, evidence includes:

- details of a current ACN, ABN, Australian Registered Body Number (ARBN) or ASX listing and public details from other Australian regulators

- prospectus documents

- minutes of meetings

- corporate memoranda

- payroll data

- contracts

- quotes or invoices for Australian contractors and suppliers.

Depending on the specific requirement and facts and circumstances of your application, additional information should be provided.

Provide an ASIC historical extract showing the entity’s principal place of business and a copy of the entity’s lease or title documents showing the location of the head office or the principal place of business.

Generally, we do not accept an accountant, solicitor or agent’s office address as evidence of the entity’s head office or principal place of business.

If the address listed on ASIC is leased or owned by another entity, advise of the relationship between the entities.

Corporate group tracing is not available for this requirement.

Example: Applicant does not have a principal place of business in Australia

XYZ Pty Ltd is seeking an exemption and has provided an ASIC search that its principal place of business is in Australia. The address listed on ASIC is owned by another entity who XYZ has stated is its accountant. XYZ has no other head office or principal place of business address for its business in Australia and has not provided any other evidence to prove that it has another address in Australia.

Because of this, XYZ has not established that it satisfies this requirement.

You’ll need to provide evidence of significant Australian management staff and office presence.

Significant management staff

Significant management staff (i.e. directors and managers) in Australia must be employed by the entity, or by a relevant group entity where corporate group tracing applies. The employment arrangements must exist at the time that liability arises.

- Entity directly employs significant management staff in Australia—evidence includes:

- a diagram of the entity’s organisational structure outlining the entity’s management staff in Australia

- information outlining how the management staff is engaged and the types of management functions they undertake in relation to the entity’s commercial activities

- evidence that the management staff is Australian-based, such as an ASIC extract or corporate documents

- corporate documents, such as

- any relevant management or service agreements

- prospectus, project documents, brochures or annual reports that outline the entity’s presence in Australia.

- Group entity in a relevant corporate group employs significant management staff in Australia—evidence includes:

- the name and ABN of this entity

- the entity’s ASIC historical extract

- a corporate structure diagram of the corporate group confined to group entities (including identifying the entity seeking the exemption and the employing relevant group entity)

- information confirming that these connections and arrangements occurred on or immediately before the liability date

- information confirming that the significant management staff are managing the commercial activities being undertaken on the land of the entity seeking the exemption

- employment details and evidence such as examples of contracts, which confirm the arrangements and the periods in which they were entered into and operated for. (See ‘Employs Australian citizens or permanent residents’ for more detail.)

Significant office presence

Provide evidence the entity has significant office presence in Australia including:

- the number of offices located in Australia

- the functions and activities being undertaken in the offices

- how those functions and activities relate to the entity’s commercial activities in Australia.

If the entity’s principal place of business address recorded with ASIC or other offices are leased or owned by another entity, also provide the details of the relationship between the entities.

If the address belongs to the entity’s solicitor or accountant for instance—and the entity does not have any other location for its business—it will likely not be considered to have a significant office presence in Australia unless alternative evidence to this effect can be provided.

Example A: The other entity is not a group entity

XYZ Pty Ltd is seeking an exemption and has provided general statements that indicate that JFL Pty Ltd is providing management services for XYZ’s commercial activities in Australia.

We request evidence supporting the connection between XYZ and JFL.

XYZ responds with:

- ASIC records showing that JFL owns 60% of the shares in XYZ’s parent as well as other ASIC records for the relevant corporate group

- copies of a management agreement between XYZ and JFL

- information advising that the entities are part of the same corporate group.

XYZ’s parent directly owns at least 90% of the shares and has voting control in XYZ. But JFL does not directly own at least 90% of the shares in XYZ’s parent and does not have voting control in XYZ.

The management services JFL is providing XYZ cannot be considered when determining if this factor has been met, regardless of the presence of the management agreement.

Example B: The other entity is not a group entity

DOF Pty Ltd is seeking an exemption and has provided general statements about how it meets the significant management staff and office presence in Australia factor.

After an information request, DOF advises:

- It is connected to an entity called RLB Pty Ltd through a common director.

- RLB has engaged an unrelated management services business called YRW Pty Ltd.

- YRW is providing the management services in relation to the commercial activities on DOF’s land.

DOF also confirms that it does not employ directly. Its director—who is not an employee—provides some strategic oversight of DOF’s commercial affairs.

The connection between DOF and RLB is unable to be considered, because they are not group entities. Therefore, RLB’s arrangements—including its engagement with YRW—is unable to be considered towards DOF’s satisfaction of this factor.

Although DOF has a common director that may provide strategic oversight of the commercial activities on its land, it does not employ significant management staff directly, including their director.

Entity as employer—evidence includes:

- payroll data that identifies the total number of employees based in Australia and the number that are Australian citizens or permanent residents

- an employee register showing the residence of the employees and whether they are Australian citizens or permanent residents

- financial statements, such as profit and loss statements, confirming employee expenses

- a sample of employment contracts between the entity and its employees, as well as information confirming that the employees are Australian citizens or permanent residents.

Group entity as employer—evidence includes:

- the name and ABN of the employing entity

- the employing entity’s current ASIC historical extract

- a corporate structure diagram of the relevant corporate group that identifies the entity seeking the exemption and the employing entity

- information confirming that these connections and arrangements were current as at the liability date

- information confirming that the employees are being engaged in relation to the commercial activities being undertaken on the land of the entity seeking the exemption.

We have used future dates in these examples.

Example: Satisfies this factor with group entity

XYZ Pty Ltd is seeking exemption from AFAD for an agreement dated 20 June 2026 to acquire land. XYZ has only made general statements about its satisfaction of this factor.

In response to an information request, XYZ provides information and evidence confirming that:

- the employing entity is DEF Pty Ltd

- DEF wholly and directly owned all the shares in XYZ as at the date of liability for transfer duty

- DEF’s employees are Australian citizens and engaged in the acquisition of the land and will engage in the development of the land.

The requirement that the entity has employees who are Australian citizens or permanent residents will be considered to be met because it is satisfied by DEF.

XYZ and DEF are group entities and DEF is a relevant group entity so its circumstances and affairs can be counted for present purposes.

Example: Not satisfied, employing entity not a relevant group entity

XYZ Pty Ltd is a professional trustee of a trust. Under a contract dated 27 August 2026, it is acquiring land to develop into 55 residential lots.

The beneficiaries of the trust are 3 unit holders. Each unit holder is a corporation that operates independently of each other and has no ownership connection to XYZ.

Before the contract date, 2 of the unit holders had entered into commercial agreements on behalf of all unit holders with a third party, LTF Pty Ltd, to manage the development of the land.

LTF’s employees oversee the residential property development activities, including engaging with contractors and suppliers.

As part of its application for the AFAD exemption, XYZ submits that LTF’s 250 employees are all Australian citizens.

Because these employees are not employed directly by XYZ—and XYZ has not established that LTF is a relevant group entity where corporate tracing is applied—LTF’s employees are not able to be counted for the purposes of the ruling. Only the circumstances and affairs of a relevant group entity, where corporate tracing is applied, can be considered in determining whether the factor is satisfied.

Entity carries on business in Australia—evidence includes:

- a list of business activities conducted in Australia in the last 5 years and evidence of this business activity

- evidence of expenditure on business activities such as invoices from third parties relating to the supply of goods or services in the relevant period

- financial or corporate documents, such as

- annual reports

- profit and loss statements

- wage or salary expenditure

- strategic plans

- incurred and forecast expenditure

- other corporate documents outlining the above.

Group entity in a relevant corporate group carries on business in Australia—evidence includes:

- the name and ABN of this entity

- this entity’s current ASIC historical extract

- a corporate structure diagram of the relevant corporate group confined to group entities (including identifying the entity seeking the exemption and the entity carrying on the business)

- ASIC historical extracts of all group entities that traces the entity seeking the exemption to this entity via corporate group tracing

- information confirming that these connections and arrangements were current as at the liability date

- information confirming that this entity’s business in Australia involves commercial activities being undertaken on the land of the entity seeking the exemption.

‘Primarily’ means chiefly or principally. Where decisions are made by multiple entities across different jurisdictions, an assessment must be made as to whether those decisions that are made by management or employees in Australia are the primary decisions about the entity’s business and operations in Australia. Generally, where more than 50% of decisions are made by management or employees in Australia, this would prima facie suggest that the requirement is satisfied. However, this is not an absolute rule; and the assessment must be made on a case-by-case basis.

Entity

To prove the entity’s management or employees in Australia primarily make decisions about the entity’s business and operations in Australia, include:

- memoranda executed by or on behalf of the entity, stating the powers of the entity’s directors, managers and key personnel in relation to Australian participation

- organisational structure identifying location and responsibilities of staff involved in making strategic or key operational decisions

- copies of minutes of meetings conducted in Australia that show Australian decision making on or immediately before the liability date. (The meeting minutes must confirm the names of the people in attendance and the decisions being made by those people.)

Group entity

To prove the management or employees of a group entity primarily makes decisions about the entity’s business and operations in Australia, include:

- the name and ABN of this entity

- this entity’s current ASIC historical extract

- a corporate structure diagram of the relevant corporate group confined to group entities (including identifying the entity seeking the exemption and the entity that conducts its commercial activities in Australia and primarily makes decisions about the entity’s business and operations in Australia)

- ASIC historical extracts of all group entities that trace the entity seeking the exemption to the relevant group entity via corporate group tracing

- information confirming that these connections and arrangements were current as at the liability date

- information confirming that this Australian decision-making relates to the entity seeking the exemption and the commercial activities being undertaken on the land of the entity seeking the exemption.

We have used future dates in this example.

Example: Unlikely to satisfy this factor

XYZ Pty Ltd is a developer that is seeking exemption from AFAD for an agreement dated 27 August 2026 to acquire land.

XYZ has stated that all important development decisions are made by Mr Diamond, who is XYZ’s chief financial controller. XYZ has provided evidence that confirms that Mr Diamond’s authority level to approve decisions is limited to administrative costs of no greater than $10,000.

Other information provided by XYZ suggests that it is entering into multiple contracts with unrelated third parties in relation to its development activities in Australia that are valued at greater than $5 million in the period before 27 August 2026.

Without further information or evidence, it is likely that Mr Diamond’s authority may not be sufficient to satisfy that decisions about the business and operations in Australia of XYZ are primarily made by management or employees in Australia.

We issue an information request seeking information about other management or employees of XYZ that could potentially better meet this factor.

FIRB requirements

Where possible, we will attempt to assess whether Foreign Investment Review Board (FIRB) requirements have been met by the information already available to us. If this is not possible, we will request supporting documentation.

You can provide relevant supporting documentation when lodging your exemption application; for example:

- where approval was required, a copy of the entity’s FIRB approval or no objection document

- where approval was not required, the reasons why and any information from FIRB from the time of acquisition supporting these reasons

- where approval has not yet been received, a copy of the FIRB application (together with supporting documents)

- copies of any other correspondence with FIRB concerning the entity’s compliance

- details regarding how any previous non-compliance issues have been addressed.

Regulatory requirements

You will need to meet general regulatory requirements, including compliance under Queensland revenue laws.

We will assess whether legal and regulatory requirements have been met by the information already available to us. If this is not possible, we will request supporting documentation.

You can provide relevant supporting documentation when lodging your exemption application; for example:

- a written statement confirming whether regulatory requirements in Australia (if applicable) or another relevant jurisdiction (if any) have been complied with

- where the entity or the group entity is listed on a stock exchange

- the stock exchange on which it is listed

- the name it is listed under

- any unique code used to identify the entity on the exchange

- the entity and the group entity’s financial or annual reports required to be lodged with ASIC (or equivalent entity) for the last 2 years (If the entity or the group entity have been registered for less than 2 years, provide a copy of the entity’s financial report and any other reports lodged.)

- if the entity or the group entity is under the control of another entity, consolidated financial reports or annual reports of the controlling entity required to be lodged with ASIC (or equivalent entity) for the last 2 years

- if relief from lodgement of financial reports has been granted by ASIC, evidence of this

- if the entity or the group entity is not registered with ASIC, any other documents (including financial reports or annual reports) for the last 2 years that the entity and the group entity are required to prepare by the law that applies in the entity’s place of origin. (If any document is not in English, provide a certified translation of that document into English.)

If you (the entity and/or the group entity) have had previous dealings with us, we will consider whether you have been subject to, or are currently dealing with audit or collection activity. To help with this process, you should provide relevant QRO client numbers.

If any revenue laws have not been complied with, provide confirmation that any previous non-compliance issues have been addressed.

Typically, we only consider information relating to the liability date; however, we may consider the entity’s and the group entity’s historical and current non-compliance.

If you have entered into a payment arrangement with us, this will not be treated as non-compliance provided you meet your responsibilities under the arrangement.

Example: Unpaid state tax liabilities

XYZ Pty Ltd is applying for an exemption and has advised that it complies with Queensland’s revenue laws, including lodging and paying all liabilities on time.

Records indicate that XYZ has outstanding unpaid state revenue liabilities spanning multiple financial years. A further search shows that it does not have an instalment plan in place to reconcile the outstanding debt.

We may ask XYZ to explain what actions or plans it will put in place to resolve the outstanding amount.

XYZ’s response—in addition to not voluntarily disclosing the outstanding amount or taking steps to reconcile the payment—will be considered when determining if it meets this requirement.

We have used future dates in this example.

Example: Subject of audit activity

ETF Pty Ltd has applied for an AFAD exemption for a relevant transaction with a liability date of 27 January 2026, which was received on 30 April 2028.

ETF submits that it has been consistently compliant with all Queensland revenue laws since it first registered on 1 January 2010. It has provided evidence that it has paid its land tax liabilities leading up to and including the 2025–26 financial year.

Our records show that ETF has been subject to an audit relating to non-compliance in Q4 of the 2025–26 financial year. ETF had failed to disclose relevant landholdings for this period, which resulted in an incorrectly reduced land tax assessment. It was uncooperative during the investigation, which resulted in 25% penalty tax and full unpaid tax interest.

Even though this non-compliance occurred after the relevant transaction, it can still be considered when determining if ETF meets the regulatory requirement.

Developer requirements

You will need to meet the developer requirements.

For this test, you need to establish that the AFAD residential land is a qualifying development. That is, the land you acquire is AFAD residential land for the purposes of undertaking a development or re-development of 20 or more residential lots on the acquired land in Queensland, and the development is primarily residential.

Generally, we look to determine whether an entity will be creating the requisite number of lots for the purposes of residential development. Evidence you can provide includes:

- the executed or draft development or redevelopment plan for the land

- relevant development approvals

- feasibility study

- application documents for council approval and town planning advice.

Example: Exemption application made before development approval

ASD Pty Ltd is acquiring land for a development of 55 residential lots. It does not yet have a development plan for the land or any development approval.

We will require evidence that ASD is acquiring the land for the purpose of developing 55 residential lots, including:

- feasibility study

- draft development plans

- application documents for council approval and town planning advice.

We have used future dates in this example.

Example: Land not acquired for a qualifying development

XYZ Pty Ltd entered into a contract to acquire AFAD residential land on 30 January 2026, with no proposed development of residential lots planned on the subject land.

In its application for the AFAD exemption for this relevant transaction, XYZ informs us that it also has made other acquisitions of AFAD residential land in which it:

- produced 300 residential lots on AFAD residential land in Queensland on 1 July 2026

- will produce a further 200 residential lots with completion due on 29 June 2027 on different AFAD residential land in Queensland.

XYZ is not able to obtain an exemption for the relevant transaction because it is not acquiring the AFAD residential land for the purpose of undertaking a development or re-development of the subject land into residential lots.

A separate application will be required for the other developments to be considered for the AFAD exemption (if applicable). The relevant transactions for the other developments can be considered in their own right depending on the date the liability for transfer duty arose for the transaction.

Where an entity is undertaking a development or redevelopment of less than 20 lots in a relevant year, the entity may still be eligible for the exemption if the development or redevelopment is approved by the Commissioner as a qualifying development.

The Commissioner will approve a qualifying development if one of the following applies.

- The development or redevelopment is significant to a non-metropolitan area regarding:

- the nature of the development and area

- the contribution made to housing stock and infrastructure in the context of population size, demographics and activity in the area

- the economic and social impacts of the development for the area

- whether in the absence of the development by the entity, such outcomes would otherwise be likely for the area

- any other relevant factors.

- The development or redevelopment is in a priority development area under the Economic Development Act 2012.

- The development or redevelopment is part of a declared coordinated project under the State Development and Public Works Organisation Act 1971.

This condition will be met where an entity, or the relevant corporate group of which the entity is a group entity, is a large developer.

A ‘large developer’ is an entity, or a relevant corporate group, that undertakes development or redevelopment of 20 or more residential lots in Queensland in a relevant 12-month period, including the land the subject of the exemption. A relevant 12-month period is a 12-month period that includes the date the liability for transfer duty arises for the land the subject of the exemption.

Generally, we look to determine whether an entity will be creating the requisite number of lots for the purposes of residential development, and whether that development will occur in the relevant 12-month period. In determining whether 20 or more residential lots have been developed or redeveloped, averaging for up to 5 consecutive years is permitted (averaging period).

Satisfying the test

You should describe how you are satisfying the test, including:

- nominating an averaging period of up to 5 consecutive financial years, which must include the date of the relevant transaction and the development of the land the subject of the exemption (where relevant)

- identifying the developments or redevelopments undertaken or to be undertaken in the averaging period

- identifying the date each development or redevelopment is planned to commence and complete in the averaging period

- identifying the number of residential lots already produced, or to be produced, from each development or redevelopment and the date the residential lots were registered, or are expected to be registered, in the averaging period.

You will also need to provide information based on whether the lots will be created before or after the date of the application, including:

- for lots created before the date of application

- evidence identifying the land to be developed and its ownership

- Titles Queensland evidence of lot creation (which may include registered plans of subdivision for the lots or the registration confirmation statement for each lot)

- for lots to be created after the date of application

- evidence identifying the land to be developed and its ownership

- evidence of the total number of residential lots to be created, such as development plans, feasibility studies, council development approvals, and the expected date for title registration.

If you propose to rely on developments by a relevant group entity, provide:

- the name and ABN of the other entity

- a current copy of the group entity’s current ASIC historical extract and evidence of voting control

- a corporate structure diagram of the relevant corporate group confined to group entities (including identifying the entity and the relevant group entity)

- information confirming that these connections and arrangements existed at material times, including the date of the liability

- information and evidence confirming the relevant group entity’s developments.

Five-year averaging methodology

The averaging period can only be for a period of up to 5 consecutive financial years and must include the date of liability. If it is proposed to include previous lot productions as well as future lot productions, the lot productions must occur within the 5-year averaging period.

Generally, ‘completion’ means the date the lots were created, such as when the plan of subdivision for the land is registered. (Titles Queensland evidence will be required.) For developments such as LLCs or ILUs, certification as to the satisfaction of the development conditions may be used as an alternative for evidencing lot creation in these circumstances.

We have used future dates in these examples.

Example: Entity satisfies the large developer test (averaging)

ABC Pty Ltd acquired land on 1 July 2026 for a development of 15 residential lots with completion expected on 30 June 2027. It is seeking eligibility under the large developer test because a development of 15 lots is not sufficient to meet the qualifying development test, and it does not meet the requirements for the Commissioner approving a qualifying development.

To satisfy the large developer test, ABC is relying on its development of 15 lots as well as their other developments.

ABC has provided information and evidence that it:

- completed the production of 20 residential lots on AFAD residential land in Queensland on 1 July 2025

- will produce a further 40 residential lots with completion due on 30 June 2028 on different AFAD residential land in Queensland.

This is the calculation for the averaging period from 1 July 2025 to 30 June 2028.

- This averaging period of 3 years includes:

- 1 July 2025, the earliest date of lot creation to be counted

- 1 July 2026, the date of the relevant transaction

- 30 June 2027, the date of expected lot creation for the land the subject of the exemption

- 30 June 2028, the latest date of lot creation to be counted.

- Total permitted residential lot count: 20 + 15 + 40 = 75

- Averaging: 75 lots ÷ 3 years = 25 lots per year

ABC has met the large developer test because it has shown that it is developing 20 or more residential lots per year, including the land the subject of the exemption.

Example: Relevant corporate group satisfies the large developer test (averaging)

DSA Pty Ltd acquired land on 1 July 2026 for a development of 15 residential lots with completion expected on 30 June 2027. Development of 15 lots is not sufficient to meet the qualifying development test, and DSA does not meet the requirements for the Commissioner approving a qualifying development.

To satisfy the large developer test, DSA is relying on its development of 15 lots. It is also relying on other developments by XYZ Pty Ltd (an entity that has wholly and directly owned DSA since 1 July 2018 by way of share-ownership with the requisite voting control, too).

DSA has provided information and evidence that XYZ:

- completed the production of 20 residential lots on AFAD residential land in Queensland on 1 July 2025

- will produce a further 40 residential lots with completion due on 30 June 2028 on different AFAD residential land in Queensland.

Neither DSA nor XYZ, or any other entity in the corporate group, are creating any other lots during this time.

This is the calculation for the averaging period from 1 July 2025 to 30 June 2028.

- This averaging period of 3 years includes:

- 1 July 2025, the earliest date of lot creation to be counted

- 1 July 2026, the date of the relevant transaction

- 30 June 2027, the date of expected lot creation for the land the subject of the exemption

- 30 June 2028, the latest date of lot creation to be counted.

- Total permitted residential lot count: 20 + 15 + 40 = 75

- Averaging: 75 lots ÷ 3 years = 25 lots per year

The relevant corporate group, comprising DSA and XYZ, has met the large developer test as it has shown that it is developing 20 or more residential lots per year, including the land the subject of the exemption.

Also consider…

- Read about build-to-rent (BTR) concessions.

- Learn about the exemption from the land tax foreign surcharge.