Relevant contracts and payroll tax

Learn what a relevant contract is and how contractor wages can incur payroll tax.

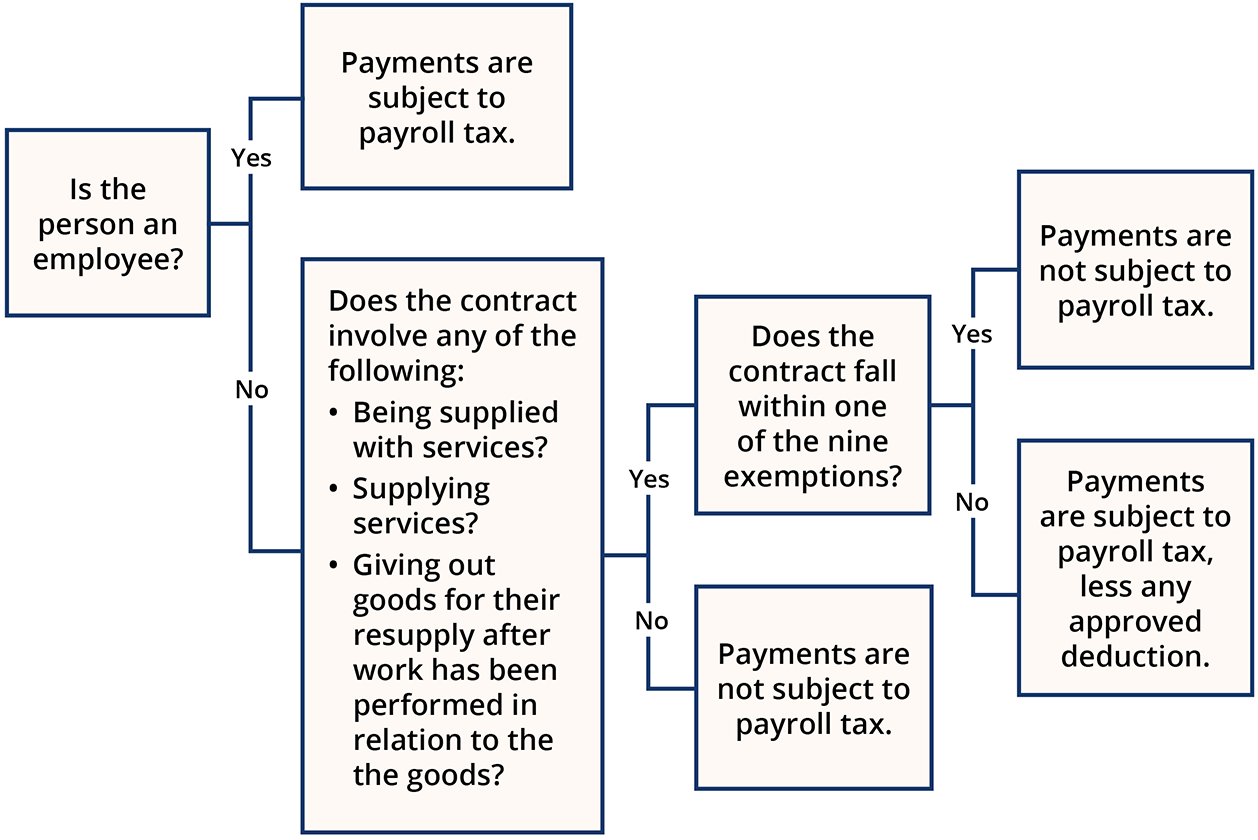

Payments you make to contractors may be taxable if your arrangement is considered a relevant contract for payroll tax purposes.

A ‘relevant contract’ is any kind of arrangement where you:

- supply services

- are supplied with services

- re-supply goods.

Re-supply means supplying goods to someone else who performs a service in relation to those goods and gives them back either in an altered form or as other goods that incorporate them.

Arrangements involving services are almost always relevant contracts, and so these contracts are taxable unless an exemption applies. There are 9 exemptions available, but you only need to satisfy one of them for your payment to be exempt from payroll tax.

If the contractor payments are taxable (i.e. no exemption applies), you may still be able to claim an approved deduction for the non-labour component (i.e. goods or materials) of the payment, depending on what type of work is being performed. You should also deduct the GST component of the payment to the contractor. Otherwise, the full payment is taxable.

Before you consider whether you are paying amounts under a relevant contract, look at whether the person providing services is your employee or whether the person’s services are provided to you by an employment agent. If you’re satisfied that neither of these apply, you can then look at whether the arrangement is a relevant contract.

You can use this flowchart to help you decide how much of your payments, if any, are subject to payroll tax.

Also consider…

- Use our interactive help as a guide to determine whether contractor provisions apply.

- Check the nexus rules for payroll tax on wages of interstate contractors and employees

- Read the public ruling on relevant contracts and medical centres (PTAQ000.6).